The History of Money

The History of Money

Free World Theory (audio time 18:22)

Click to Play

Bernard, the Terrorist

Decentralization is causing already changes to society which are profound. To illustrate how profound, here’s an example — the technology of money.

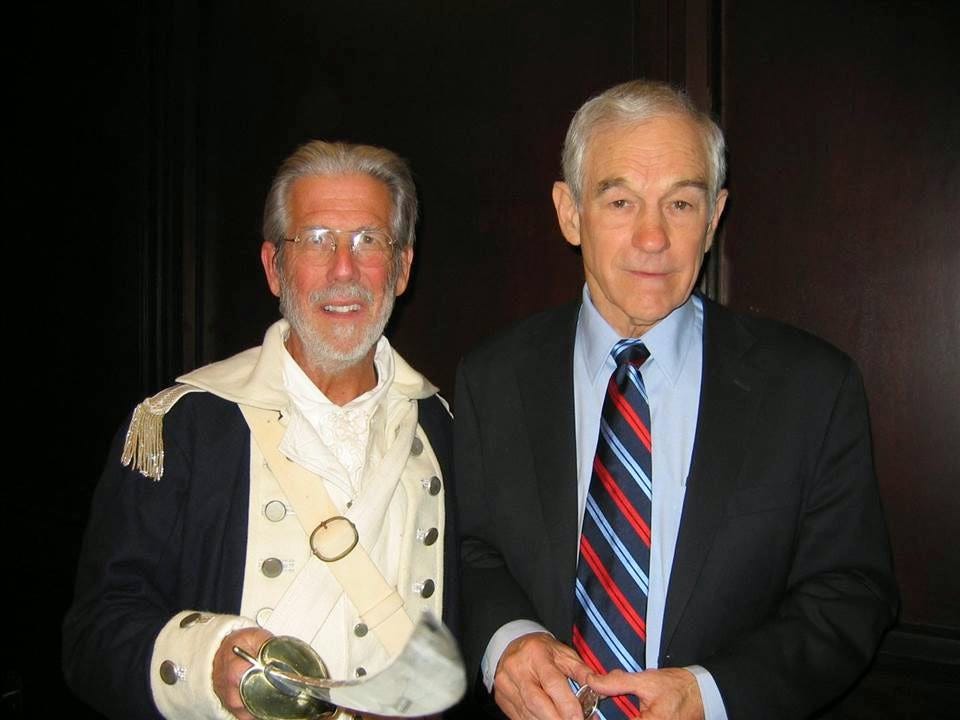

Back in 2007, US federal agents raided the home of a guy named Bernard Nothaus. They seized 500 pounds of silver and gold coins and bills he called “Liberty dollars. These were privately minted coins and printed bills with a picture of US Congressman, Ron Paul, stamped on them.

When he created his currency, Nothaus wanted to do two things. First, he wanted to promote Ron Paul’s presedential campaign. Second, he wanted to show that Americans would flock to gold and silver-backed currency if it was available.

He wasn’t the only one to create alternate currencies. There were a number of private currencies in use in the US at the time.

There were “Phoenix Dollars,” named after the mythical bird.

There were “Ithica Hours,” a cuurrency used and highly prized by people in Ithica, New York.

There were “B-Notes,” a currency used in Baltimore, Maryland, and more.

But Liberty Dollars were getting dangerous to the establishment. Libertarians all over the country were talking about them. They said, they were better than Federal Reserve Notes, which are a fiat currrency. So Bernard Nothaus was arrested.

At his trial, the prosecuting attorney for the government said, Nothaus had committed, “a unique form of domestic terrorism by trying to undermine the legitimate currency of the United States.”

The Coming of Bitcoin

In 2009, two years after Bernard Nothaus was arrested for creating “Liberty Dollars,” a shadowy figure who called himself “Satoshi Nakamoto” released onto the internet something the world had never seen before. It was a new technology. It was called “Bitcoin.”

Bitcoin was a new kind of money — the world’s first crypto-currency.

There was a small, loosely connected group of people who had been working on the idea for years. Nick Szabo, Hal Finney, Charlie Shrem, Roger Ver, and more. The Satoshi — nobody knew who he really was — released Bitcoin.

At first, it was just a novelty for these tech guys. But word spread, and more and more people began experimenting with it — because Bitcoin was a fascinating toy.

It had negligable monetary value at first. It was just a mathematical novelty. Then in 2010, the first purchase ever made with Bitcoin happened when a programmer offered 10,000 Bitcoin for two pizzas.

He posted this message online: “I’ll pay 10,000 Bitcoin for a couple of pizzas. Like maybe two large ones so I have some left over for the next day. I like having left over pizza to nibble on later.”

Another programmer, a teenager named Jeremy Sturdivant, took him up on the offer. He accepted the 10,000 Bitcoin and sent two large Papa John’s pizzas. It was the first purchase ever made with Bitcoin.

Two pizzas — worth about $20.00 in US currency at the time.

Today, as I record this, 10,000 Bitcoin is worth over 550 million dollars. The all time high price of one Bitcoin is about 64 thousand dollars, reached in April, 2021.

And Papa Johns pizza has begun using the image of Bitcoin in its ad campaigns.

In the Beginning

Author, Jack Weatherord, in his book The History of Money, tells the story of a young Somali woman, in the year 2001.

She lives in a straw and mud hut.

She has two kids. She owns two goats for milk and some chickens for eggs. Once a week, she fills one of those large jugs with milk, floats the eggs in the milk so they won’t break, balances the jug on her head and walks 11 miles to an open-air marketplace.

There, she trades for whatever she can get — bread, flour, clothes for her kids.

At the end of the day, she walks 11 miles back home with her kids in the dark.

The next week, she does exactly the same thing. This is her entire life.

This is how a barter economy works. It’s cruel, and unproductive. It takes all the time you have just to get a little food and few things to survive. Five thousand years ago, this is how everybody lived.

They had no choice because money hadn’t been invented yet.

Barter is inefficient — it takes a lot of energy to acquire just a little property.

If centralized state fiat currencies should fail, and so-called civilized nations were reduced to barter, it would be an environmental and human catastophe.

The First Money

Around 4,000 years ago, things changed. The first money appeared in the form of gold and silver ingots.

Using ingots, trade grew more efficient. Instead of carrying your bulky stuff around, you could carry small lumps of metal, and trade those. The ingots SYMBOLIZED property.

The first ingots were called “shekels” or “talents,” and you had to weigh them every time you made a trade because there were no standard sizes.

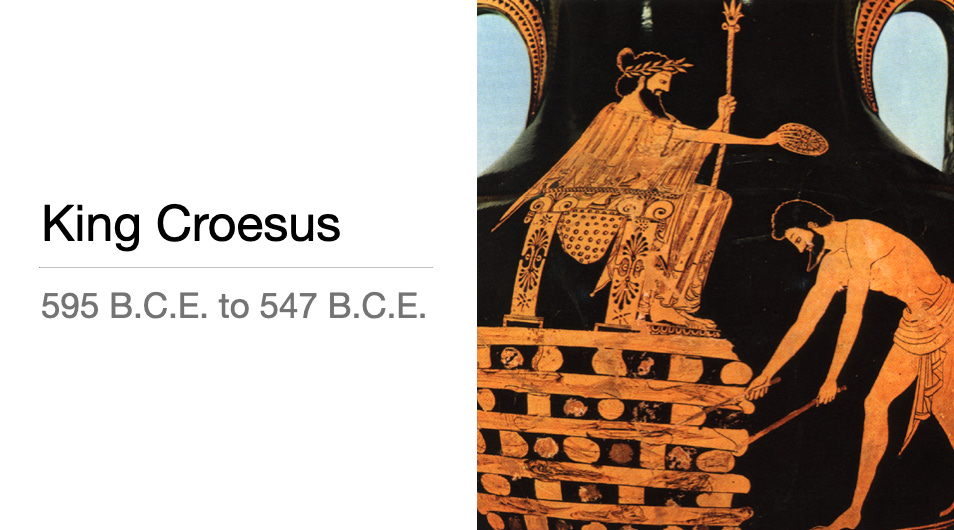

This crude money system stayed in place for thousands of years, until around 600 B.C.E.

Then, in a Greek city-state called Lydia, under King Croesus, a new technology appeared: coins.

These were different from a lumpy ingot — they were small, flat, circular coins with a standardized size and weight. The lion on it was the king’s official seal.

Because they had a standardized weight and size, coins made trading more efficient, again. So efficient, in fact, that Lydia became a rich trading center and a tourist attraction for the whole Greek world.

Lydian coins created the first permanent marketplace. A shopping district. Where one shop sells chickens. Another grain. Another sells jewelry, and so on. Standardized coins changed the primitive marketplace into real commerce for the first time.

Lydia had the first brothels. The first gambling.

It became the wealthiest place in ancient Greece. Like Las Vegas — a must see spot.

Coin money made the organization of society possible on a much grander scale than ever before.

As a result, within a hundred years, coin money spread all around the Greek world.

The Roman Empire

A few hundred years after King Croesus, Rome discovered coin money had a new and more insidious kind of power.

The Romans were conquerors, and they used coins to impose one standard money system throughout the whole known world so they could collect standard taxes.

In its beginning, Rome expanded by looting all its wealthy neighbors and bringing riches, especially gold and silver, back to the capital.

Once conquered, a town could keep its local Gods – but not their money system. Coins stamped with Roman symbols told the vanquished people who was in control.

When Caesar was conquering towns, it’s said one of his great achievements was building Roman mints along the way so standard coinage could be imposed, immediately.

Rome, itself, produced nothing. It just took over places that did. All Rome had to offer was bureaucracy and military administration.

It could expand as long as there were new rich territories to conquer and loot. But by around 1 C.E., the time of Tiberius (and the empire), all the easy territories had been taken. So they tuned to taxation, which quickly became severe. They also turned to money inflation.

Today, we tend to think Rome was great because it had a great military. But it wasn’t the military that held the empire together, it was the money. The technology of forced standardized coinage enabled Rome to be the biggest empire the world had ever seen.

When they killed their money system by making coins out of cheap metal, they killed Rome.

Diocletian and Constantine tried to fix the empire by turning to religion. It didn’t work. They should have fixed the money system.

Rome had spread its coinage to every corner of Europe and when the money system collapsed, trade stopped, and Europe broke up into the isolated city-states that we now call the Dark Ages.

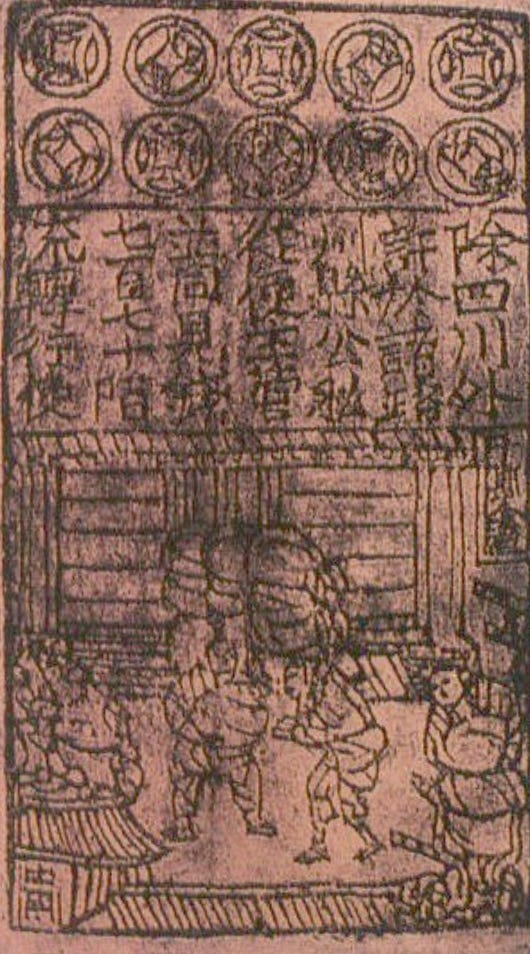

Then Came Paper

The first paper money appeared in China, around 200 C.E. It never spread beyond China, even though Marco Polo reported it was still being used a thousand years later in the 1300s.

In the west, paper money wasn’t possible until printing was invented by Guttenberg in 1450.

The first national experiment in paper money was in France, two-and-half centuries later, in 1715.

A Man named John Law got permission from the French government to issue paper money. He then bragged to his friends that he could make gold by simply printing it. And he printed paper money like crazy.

Within four years he’d created the world’s first runaway inflation.

There’s a political cartoon from the era — it shows the monarchy feeding John Law who is defecating money — and the people are grabbing it.

It was the Americans, 60 years later, who created the first successful paper money. The American Revolution was the first time that paper money was again printed on a national scale. In fact, it financed the revolution.

The currency was known as “Continentals.”

By the end of the revolution, the Continental Money System had gone broke, and Americans were disgusted by it. Americans thought it was a failure.

But other nations looked at paper money as a great success – because the Americans had won the war against the British by using the novel technique of printing money out of thin air.

These experiments by the French and the Americans showed how paper money carried with it great potential — and potential danger.

It’s greatest danger was easy inflation.

Embezzling Made Easy

“Inflation” means going to the printing press and printing excess money.

There’s nothing mysterious about it — a government has a monopoly on printing printing money, so it prints up some extra for themselves because “Whose going to know?” It’s embezzling.

It works so well, they get addicted to the process. And when you print up money on a massive scale, you put so much of it in circulation, it’s becomes worthless.

It’s supply and demand — when there’s a lot of something around, its value drops.

Paper money allowed political states to embezzle on a scale never before imagined. Take for example, what happened in the Weimar Republic in 1923.

After World War One, European nations demanded that Germany pay for damages: five million dead, four thousand ruined towns, twenty thousand ruined businesses.

Germany was ordered to pay 130 Billion Gold Marks – which was impossible. It just turned Germany into a slave state.

So in protest, German bureaucrats turned to hyper-inflation. Money became so cheap, it stopped functioning as a money. It became nothing but litter on the street.

Here’s a passage from a book called Before the Deluge by Otto Friedrich. It’s from an interview with an economist who lived through that era:

ECONOMIST: “You must understand that the German universities had cut themselves off from classical economics fifty years earlier. They developed instead what was called “the historic school” of economics. This dominated the universities where all the economists were trained. I tell you, in all of Germany, there were only three teachers who really understood economics, and two of them were not even full members of their faculties.”

INTERVIEWER: “But somebody must have seen that the prevailing economic theories weren’t working.”

ECONOMIST: “Yes, of course. But the wrong theory was very handy for two important groups. First, those who didn’t want to pay the reparations, who thought it was their patriotic duty to destroy Germany’s capacity to pay. And second, the large-scale businessmen, people who financed their businesses through large-scale borrowing – who could pay off their loans with worthless money.”

As I record this is 2021, after creating trillions of dollars in so-called “stimulus money,” it’s likely the US will be entering a similar infationary era.

How to Change Civilization

Money is a technology. Just like any other, and we’ve all seen how new technologies change the world. A few recent examples…

Every one of these technologies completely reorganized civilization.

Money is a technology, like these. Except for one thing: it’s the most fundamental technology there is. Every aspect of society is organized around money.

When coin money was created in 600 B.C.E., it created commerce.

Rome became the greatest empire in the world because of the technology of money.

Today, we have digital money. It’s easier than ever for governments to inflate the currency. They don’t even have to use a printing press.

As a result, the U.S. alone has a $30 trillion debt. That’s like paper money inflation on crystal meth. A debt that size wouldn’t be possible if not for the technology of digital money.

And now, money has fundamentally changed, once again — cryptocurrencies.

Can you see how profound that is?

Economists criticize cryptocurrencies. They say, “There’s nothing backing these things up, like Gold or Silver.”

There’s nothing backing up government fiat currencies, either.

Ten years ago, when when Bernard Nothaus started a private money system, the FBI could arrest him, seize all his assets, and continue to control the game.

But not any more.

Terrific & most complete history of money.

Even a dentist could understand it

BTW, is this one available in audio format?